Fillable Nyc 400 Form in PDF

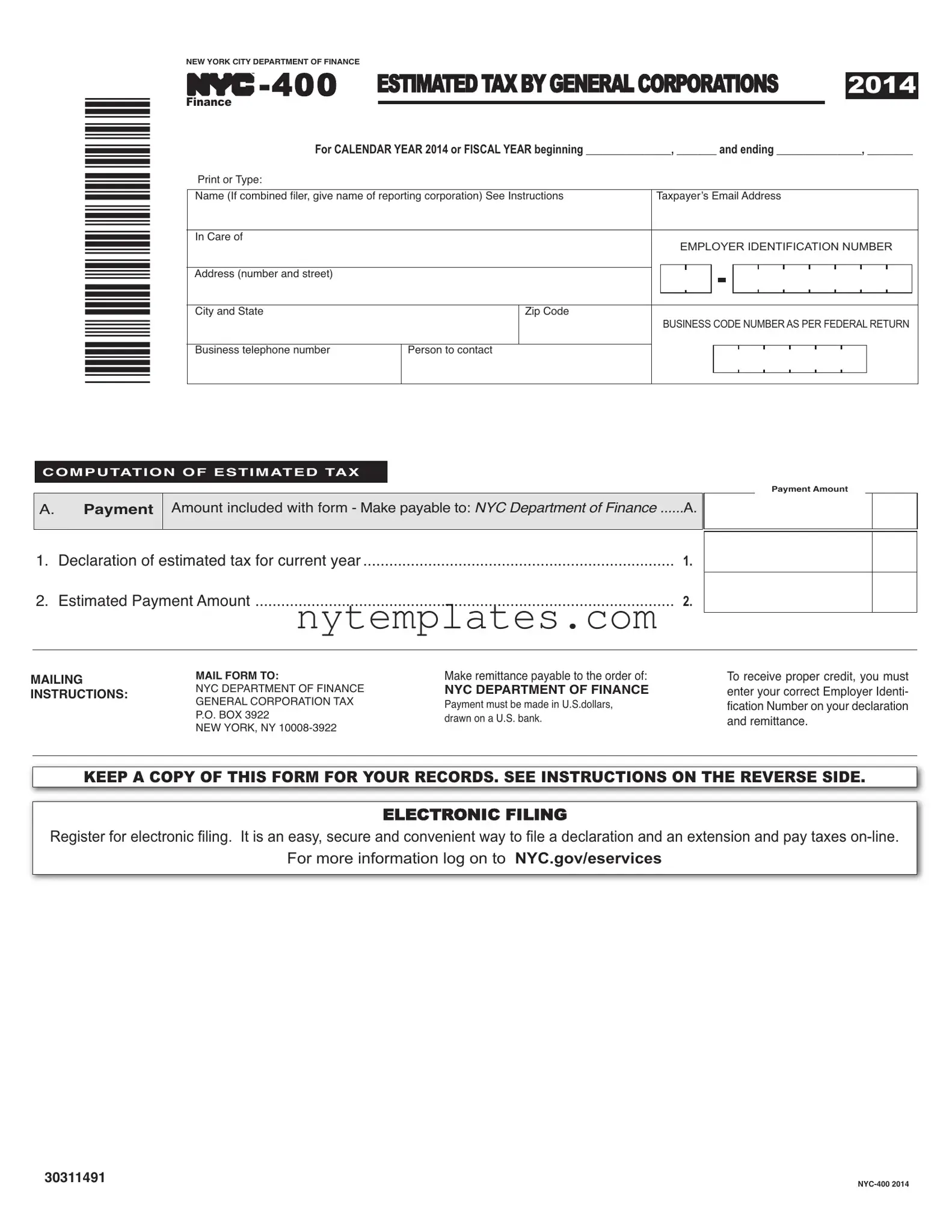

The NYC-400 form is a crucial document for corporations operating within New York City that are subject to the General Corporation Tax. This form serves as a declaration of estimated tax liability for the current year, and it is mandatory for any corporation expecting to owe more than $1,000 in taxes. When filling out the NYC-400, taxpayers must provide essential information such as their business name, Employer Identification Number (EIN), and contact details. The form requires an estimated payment amount, which is calculated based on the corporation's tax liability from the previous year. For those filing a combined return, the group member responsible for the filing must complete this form. It is important to note that corporations must adhere to specific due dates for estimated tax payments, which are outlined in the instructions accompanying the form. Additionally, the NYC-400 can be amended if necessary, and late filing may result in penalties. To streamline the process, electronic filing is available and is recommended for its convenience and security. Understanding the requirements and deadlines associated with the NYC-400 is essential for compliance and to avoid potential penalties.

Preview - Nyc 400 Form

*30311491*

NEWYORK CITYDEPARTMENT OF FINANCE

TM |

ESTIMATEDTAXBYGENERALCORPORATIONS |

2014 |

||||||||||||||||||||||

FINANCE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For CALENDAR YEAR 2014 or FISCAL YEAR beginning _______________, _______ and ending _______________, ________ |

||||||||||||||||||||||||

Print or Type: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Name(If combined filer, give name of reporting corporation) See Instructions |

Taxpayer’s EmailAddress |

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In Care of |

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER |

|||||||||||||||||||

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address (number and street) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City and State |

|

|

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

BUSINESS CODE NUMBER AS PER FEDERAL RETURN |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business telephone number |

|

Person to contact |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPUTATION OF ESTIMATED TAX

Payment Amount

A.Payment

Amount included with form - Make payable to: NYC Department of Finance |

......A. |

|

|

|

|

|

|

|

|

|

|

1. |

Declaration of estimated tax for current year |

1. |

2. |

Estimated PaymentAmount |

2. |

MAILING INSTRUCTIONS:

MAILFORM TO:

NYC DEPARTMENT OF FINANCE GENERAL CORPORATION TAX P.O. BOX 3922

NEW YORK, NY

Make remittance payable to the order of:

NYC DEPARTMENT OF FINANCE

Payment must be made in U.S.dollars, drawn on a U.S. bank.

To receive proper credit, you must enter your correct Employer Identi- ficationNumberonyourdeclaration and remittance.

KEEP A COPY OF THIS FORM FOR YOUR RECORDS. SEE INSTRUCTIONS ON THE REVERSE SIDE.

ELECTRONIC FILING

Registerforelectronicfiling.

For more information log on to NYC.GOV/ESERVICES

30311491

Form |

Page 2 |

|

|

WHOMUSTFILE

Every corporation subject to the NewYork City General CorporationTax (Title 11, Chapter 6, Subchapter 2 of theAdministrative Code) must file a declaration

NOTE:Ifthecurrentyear’staxisreasonablyestimatedtoexceed$1,000,anestimatedpaymentisrequiredevenifthisisthefirstyearofbusi- nessinNewYorkCityforthetaxpayerorthetaxpayerpaidonlytheminimumtaxfortheprecedingyear.Failuretopayorunderpayment ofestimatedtaxinthesecircumstanceswillresultinpenalties.

LINE1 - DECLARATIONOFESTIMATEDTAXFORCURRENTYEAR

Corporationswhosetaxliabilityfortheprecedingyearexceeds$1,000arerequiredtopay,withthetaxreportfortheprecedingyearorwith theapplicationforextensionoftimeforthefilingofsuchreport,25%ofthetaxliabilityfortheprecedingyearasafirstinstallmentofes- timatedtaxforthecurrentyear. Aftertakingcreditforthat25%paymentandfortheamountofanyoverpaymentshownonlastyear’sre- turnwhichthetaxpayerelectedtohaveappliedasacreditagainstthecurrentyear’stax,taxpayersfilingestimatedtaxarerequiredtopay the balance of estimated tax in fractional installments.

ESTIMATEDTAXDUEDATES

Iftherequirementsforfilingestimatedpayments |

Filetheformonorbeforethe: |

Thebalanceofestimatedtaxisdueasfollows: |

arefirstmetduringthetaxableyear: |

|

|

|

|

|

Before the first day of the 6th month |

15th day of the 6th month |

l 1/3 by the 15th day of the 6th month |

|

|

l 1/3 by the 15th day of the 9th month |

|

|

l 1/3 by the 15th day of the 12th month |

|

|

|

On or after the first day of the 6th month and before the |

15th day of the 9th month |

l 1/2 by the 15th day of the 9th month |

first day of the 9th month |

|

l 1/2 by the 15th day of the 12th month |

|

|

|

On or after the first day of the 9th month and before the |

15th day of the 12th month. In lieu of this form, |

Pay in full |

first day of the 12th month |

a completed tax report, with payment of any unpaid |

|

|

balance of tax, may be filed on or before the 15th day |

|

|

of the 2nd month of the following year. |

|

|

|

|

If any of the above dates fall on a Saturday, Sunday or legal holiday, the due date is the next business day.

AMENDMENTS

LATEFILING

PENALTY

The law imposes penalties for failure to pay or underpayment of estimated tax. (Refer to Section

istrative Code.)

ELECTRONICFILING

Note: Register for electronic filing. It is an easy, secure and convenient way to file and pay an extension

For more information log on to NYC.gov/eservices

Form Characteristics

| Fact Name | Details |

|---|---|

| Purpose of NYC-400 | The NYC-400 form is used by corporations to declare estimated tax payments for the New York City General Corporation Tax. |

| Filing Requirement | Every corporation subject to the General Corporation Tax must file the NYC-400 if its estimated tax exceeds $1,000. |

| Governing Law | This form is governed by Title 11, Chapter 6, Subchapter 2 of the New York City Administrative Code. |

| Payment Instructions | Payments must be made in U.S. dollars and drawn on a U.S. bank, payable to the NYC Department of Finance. |

| Estimated Tax Definition | Estimated tax is the amount a taxpayer expects to owe, calculated as per Section 11-603 of the Administrative Code. |

| First Installment Requirement | If the prior year's tax liability exceeded $1,000, a first installment of 25% is required with the tax report or extension application. |

| Due Dates | Due dates for estimated tax payments vary based on when the filing requirement is met during the taxable year. |

| Amendments | An amended NYC-400 should be filed if corrections are needed to the tax estimate or related payments. |

| Late Filing Penalties | Filing the NYC-400 late results in all installments becoming due immediately, with penalties imposed for underpayment. |

| Electronic Filing | Corporations can register for electronic filing, which is a secure and convenient method for submitting the form and making payments online. |

More PDF Templates

New Birth Certificate - Applications must include the applicant's relationship to the deceased and the reason for requesting the certificate.

Nyc Pba 14 - The form includes a section for dentist remarks and office use, ensuring a thorough review process by the PBA funds office.